$450,000 – Habitat will originate mortgages at 0% interest for 24-30 years

Not currently accepting applications

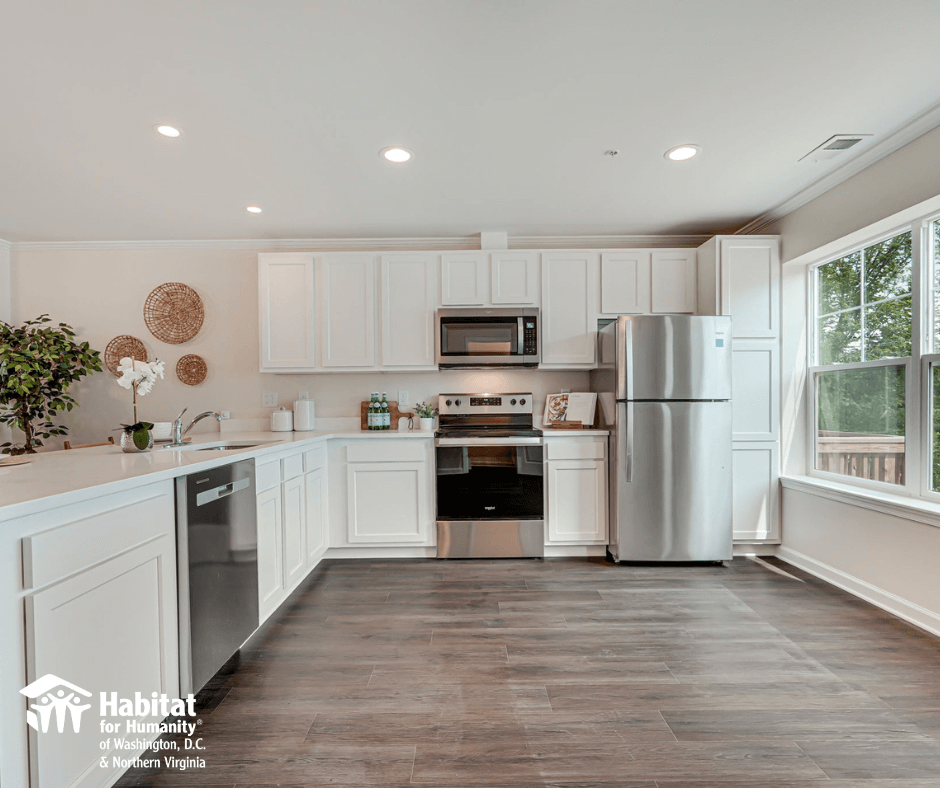

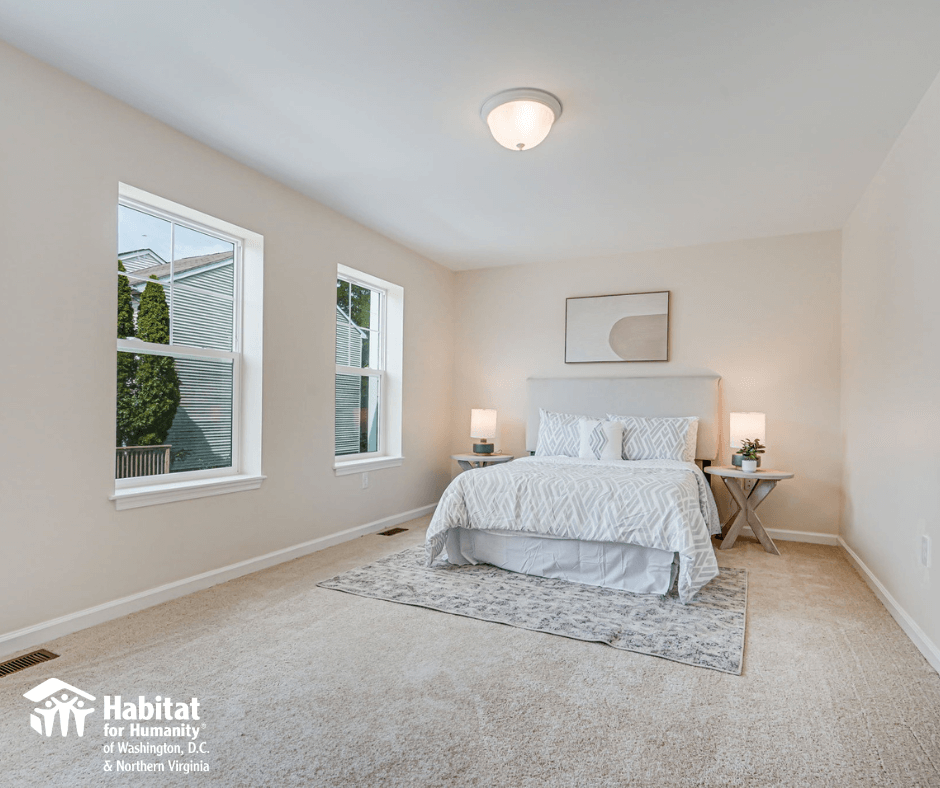

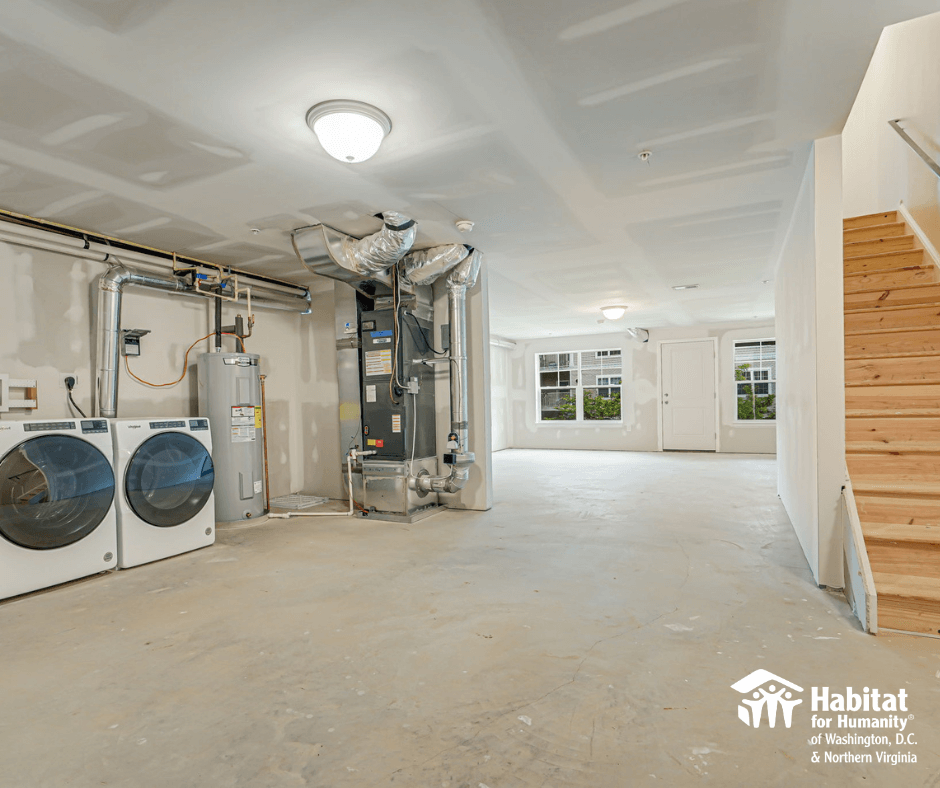

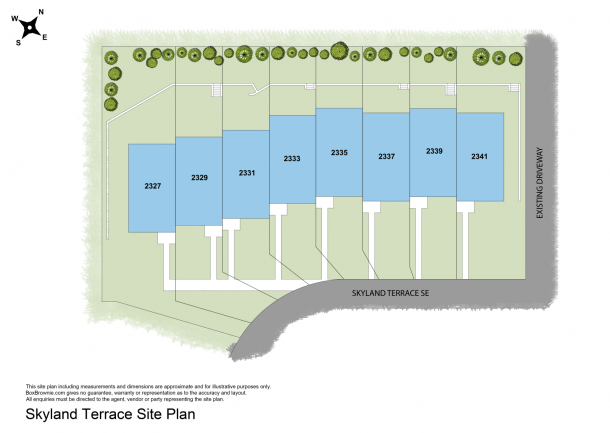

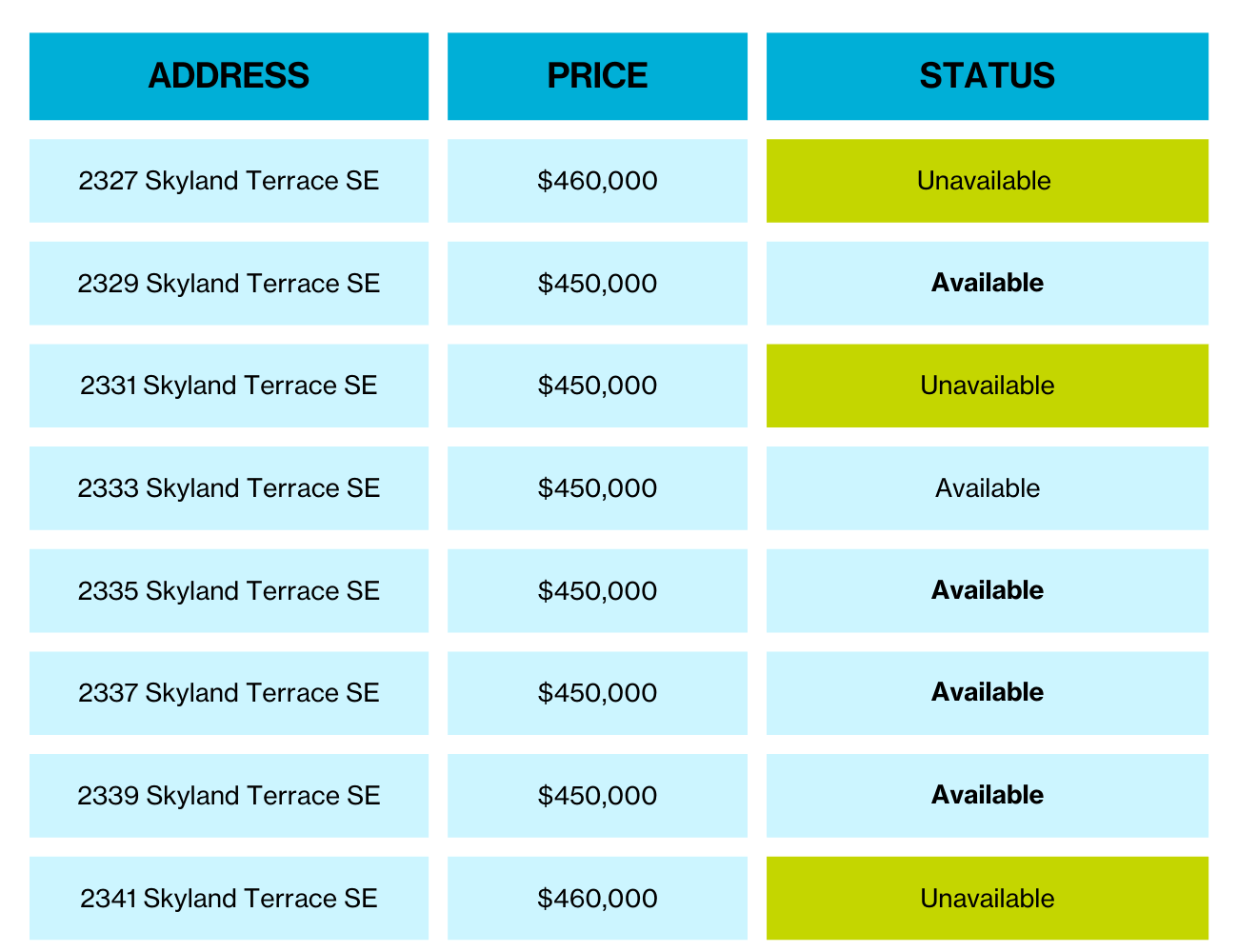

Welcome to the Towns of Skyland Terrace! Spacious 3-bed, 2.5-bath homes with 1545 sq ft of living space in the sought-after DC area. Benefit from energy-efficient appliances, windows, and insulation for lower utility costs. Discover beautiful features like maple cabinets, granite countertops, and ceramic finishes in the bathrooms. Each unit comes complete with a washer and dryer. The low-maintenance brick and hardi-board exteriors ensure durability.

Enjoy comfort, style, and affordability in this vibrant DC community.

The Towns of Skyland Terrace are developed by Habitat for Humanity of Washington D.C. & Northern Virginia (Habitat DC-NOVA). This community was made possible in part by a partnership with Douglass Community Land Trust. That means that the land will belong to the Land Trust, and the home will belong to the homeowner. This allows the home to cost less and remain affordable forever, while the homeowner can still gain equity from the sale of the home. Learn more about the Douglass Community Land Trust.

Please watch our orientation video to learn more about the homes, the Habitat Homeownership program, and how to apply.

For additional questions, please get in touch with Kamilla Scott, Family Services Coordinator, at kamilla.scott@habitatdcnova.org.

Skyland Towns is an Affordable Ownership Community

All homes in the community have affordability covenants, and maximum income limits apply. To qualify for purchasing these properties, a minimum family size of three and a median family income (MFI) of 30-60% are required.

Watch Orientation Video & Review Eligibility Requirements

Watch this helpful video that walks you through all the eligibility requirements. You can also review the qualifications for the homes at Skyland Terrace.

First-time homebuyer (having not owned real estate in the last 3 years)

Minimum household size of 3

No household member on the sex offender registry

Primary residency or at least one applicant with full-time employment in DC, Alexandria, Falls Church, Fairfax, Fairfax County, or Arlington County for the last 12 months or more

Total household income falls between 30-60% of Median Family Income (MFI) as defined annually by the U.S. Department of Housing and Urban Development. The 2024 limit was $154,700.

And meet at least one of the following need-based requirements:

Unsafe surrounding environment

Residing in temporary housing

Living in subsidized housing or participating in a housing voucher program

Overcrowding

Rent burden (paying more than 30% of monthly income on rent)

Heating, electrical, plumbing, or structural deficiencies

Ability to Pay:

Purchasers must meet all of the following:

If wages or salary are primary sources of income, a 2-year work history that includes a minimum of 6 months with the current employer and any gaps in employment must be explained

If self-employed, must have 2 years of documented, stable income with the last 6 months in the same line of work

Income can reasonably be expected to continue for 3 years or more

Current credit reports free of unpaid collection, judgment, and liens

Current credit reports must not show bankruptcy in the last 3 years or foreclosures in the last 7 years

Tri-Merge middle credit score of 620+

Quality for non-subprime or approved alternative third-party financing

Total debt to income ration, including new housing cost must be less than 43% of your monthly income

Show at least $2000 in current bank statements, no account overdrafts in the last two months, and bank statements or proof of assets not to exceed 10% of the fair market value

Willingness to Partner:

Douglass CLT and Habitat DC-NOVA want to ensure that people who are normally priced out of homeownership have an opportunity to build some equity while keeping the home affordable for the next buyer. When (and if!) Skyland homeowners sell their house, the new price will be calculated so that they gain financially, but the home is still affordable to someone at a similar income level.

All program participants must complete 200 hours of “sweat equity,” or volunteer work. This may include working on the construction site, attending homeownership and financial literacy classes, and/or volunteering in the office or at special events.

In accordance with Federal, State, and Local Fair Lending Laws, Habitat DC-NOVA does not maintain a waiting list of applicants and does not discriminate on the basis of race, color, national origin, religion, sex, disability, familial status, elderliness, source of funds, sexual orientation, gender identity, military status or marital status. The number of applicant households approved for Habitat DC-NOVA home ownership is driven by the availability of developed properties.